What is the Construction Industry Scheme (CIS)

Under the Construction Industry Scheme (CIS), contractors deduct money from a subcontractor’s payments and pass it to HMRC

The deductions count as advance payments towards the subcontractor’s tax and National Insurance. The subcontractor includes deductions on their self assessment tax return and they are offset against the liability due. If the deductions are higher than the liability due, HMRC will issue a repayment for overpaid tax

Contractors must register for the scheme. Subcontractors don’t have to register, but deductions are taken from their payments at a higher rate if they’re not registered.

CIS covers most construction work to:

- a permanent or temporary building or structure

- civil engineering work like roads and bridges

For the purpose of CIS, construction work includes:

- preparing the site, eg laying foundations and providing access works

- demolition and dismantling

- building work

- alterations, repairs and decorating

- installing systems for heating, lighting, power, water and ventilation

- cleaning the inside of buildings after construction work

Exceptions:

You don’t have to register if you only do certain jobs, including:

- architecture and surveying

- scaffolding hire (with no labour)

- carpet fitting

- making materials used in construction including plant and machinery

- delivering materials

- work on construction sites that’s clearly not construction, eg running a canteen or site facilities

Contractors

You must register as a contractor with the Construction Industry Scheme (CIS) if:

• you pay subcontractors to do construction work

• your business does not do construction work but you usually spend more than £1 million a year on construction

You may be a sole trader, in a partnership or own a limited company.

Rules you must follow:

- You must register for CIS before you take on your first subcontractor.

- You must check if you should employ the person instead of subcontracting the work. You may get a penalty if they should be an employee instead.

- Check with HMRC that your subcontractors are registered with CIS (known as verification)

- When you pay subcontractors, you’ll usually need to make deductions from their payments and pay the money to HMRC. Deductions count as advance payments towards the subcontractor’s tax and National Insurance bill.

- You’ll need to file monthly returns and keep full CIS records – you may get a penalty if you do not.

- You must let HMRC know about any changes to your business.

Mainstream contractors

If your business is construction and you pay subcontractors for construction work, you’re a ‘mainstream’ contractor. This applies if you’re a:

- builder

- labour agency

- gangmaster (or gang leader)

- property developer

Deemed contractors

You count as a ‘deemed’ contractor if your business does not do construction work but you spend an average of more than £1 million a year on construction in any 3-year period. This could apply to:

- housing association or arm’s length management organisations (ALMOs)

- local authorities

- government departments

Exceptions for contractors

CIS does not apply if your work is:

- paid for by a charity or trust

- paid for by a governing body or head teacher of a maintained school on behalf of the local education authority

- on the subcontractor’s own property and worth less than £1,000 excluding materials – you must call the CIS helpline to get an exemption

CIS also does not apply if you’re a deemed contractor paying for:

- work on property (that is not for sale or rent) for your own business use

- a construction contract worth less than £1,000 excluding materials – you must call the CIS helpline to get an exemption

Technical guidance for contractors:

Subcontractors

You should register as a subcontractor with the Construction Industry Scheme (CIS) if you work for a contractor and you’re one of the following:

- self-employed

- the owner of a limited company

- a partner in a partnership or trust

Under CIS, a contractor must deduct 20% from your payments and pass it to HMRC

These deductions count as advance payments towards your tax and National Insurance bill.

If you do not register for the scheme, contractors must deduct 30% from your payments instead.

If you do not want deductions to be made in advance by contractors, you can apply for ‘gross payment status’. You can do this when you register for CIS.

You do not need to register for CIS if you’re an employee. Check your employment status if you’re not sure www.gov.uk/employment-status

Technical guidance for subcontractors:

Call HMRC CIS Helpline if you have a general query about the Construction Industry Scheme.

Telephone:

0300 200 3210

Outside UK:

+44 161 930 8706

Opening times:

Our phone line opening hours are:

Monday to Friday: 8am to 6pm

Closed on weekends and bank holidays.

VAT domestic reverse charge for supplies of building and construction services

From 1 March 2021 the domestic VAT reverse charge must be used for most supplies of building and construction services.

The charge applies to standard and reduced-rate VAT services:

- for individuals or businesses who are registered for VAT in the UK

- reported within the Construction Industry Scheme

What is the VAT domestic reverse charge?

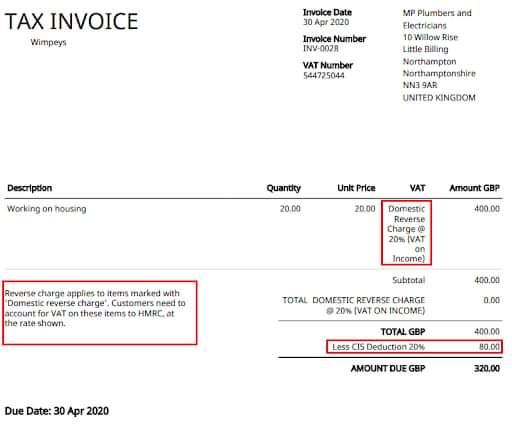

From 1st March 2021, any VAT registered sub-contractor operating within a chain of suppliers will issue their VAT invoices without any VAT charge and include a message giving the relevant information on the reverse charge.

Invoices for services that fall within the domestic reverse charge for VAT should contain the wording that the invoice is subject to a reverse charge for VAT. The invoice should also show how much VAT is due under the domestic reverse charge but this should NOT be included in the final amount

The domestic reverse charge doesn’t apply at the end of the supply chain, with the end user as VAT is charged to the end user as normal

As the supplier is not charging VAT, they do not include this on the VAT return, “VAT due on sales” (box 1) but do include the net value in “total value of sales” (box 6)

The customer of the supplier, who is receiving the services, must enter the VAT element on their own VAT return in both “VAT due on sales” (box 1) and “VAT reclaimed” (box 6) and would also enter the net value in “total value of purchases” (box 7)

In simple terms, the domestic reverse charge for VAT means that customers receiving a service will pay the VAT directly to HMRC instead of to the supplier. At the same time their reclaim for VAT paid will offset this.

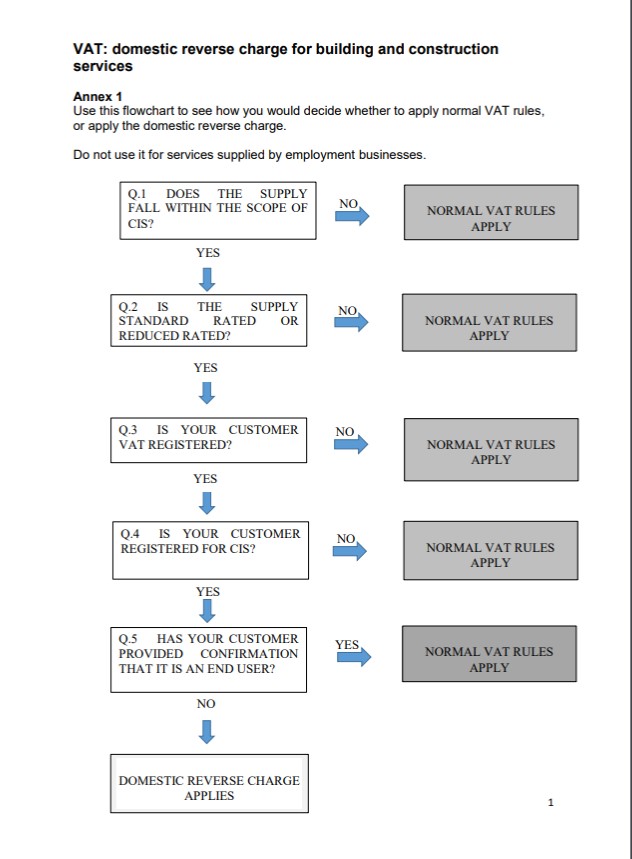

When you must use the reverse charge

You must use the reverse charge for the following services:

- constructing, altering, repairing, extending, demolishing or dismantling buildings or structures (whether permanent or not), including offshore installation services

- constructing, altering, repairing, extending, demolishing of any works forming, or planned to form, part of the land, including (in particular) walls, roadworks, power lines, electronic communications equipment, aircraft runways, railways, inland waterways, docks and harbours, pipelines, reservoirs, water mains, wells, sewers, industrial plant and installations for purposes of land drainage, coast protection or defence

- installing heating, lighting, air-conditioning, ventilation, power supply, drainage, sanitation, water supply or fire protection systems in any building or structure

- internal cleaning of buildings and structures, so far as carried out in the course of their construction, alteration, repair, extension or restoration

- painting or decorating the inside or the external surfaces of any building or structure

- services which form an integral part of, or are part of the preparation or completion of the services described above – including site clearance, earth-moving, excavation, tunnelling and boring, laying of foundations, erection of scaffolding, site restoration, landscaping and the provision of roadways and other access works

When you must not use the reverse charge

Do not use the charge for the following services, when supplied on their own:

- drilling for, or extracting, oil or natural gas

- extracting minerals (using underground or surface working) and tunnelling, boring, or construction of underground works, for this purpose

- manufacturing building or engineering components or equipment, materials, plant or machinery, or delivering any of these to site

- manufacturing components for heating, lighting, air-conditioning, ventilation, power supply, drainage, sanitation, water supply or fire protection systems, or delivering any of these to site

- the professional work of architects or surveyors, or of building, engineering, interior or exterior decoration and landscape consultants

- making, installing and repairing art works such as sculptures, murals and other items that are purely artistic signwriting and erecting, installing and repairing signboards and advertisements

- installing seating, blinds and shutters

- installing security systems, including burglar alarms, closed circuit television and public address systems

Treatment of existing contracts invoiced prior to 1st March 2021 but paid after this date:

| Date Invoice Raised | Date payment made | VAT Treatment |

|---|---|---|

| Before 1 March 2021 | On or before 31 May 2021 | Normal VAT rules |

| Before 1 March 2021 | On or after 1 June 2021 | Domestic reverse charge |

| On or after 1 March 2021 | On or after 1 March 2021 | Domestic reverse charge |

Those already mandated or voluntarily using MTD software should find that your software provider is ready for the change and will have enabled new sales codes to help you raising invoices and submitting your VAT return accurately

Example Invoice: